Or: How a Nation With More Land Than Sense Managed to Price Out Its Future

So it goes.

Listen: Canada is committing a slow, bureaucratic suicide, and we’re all standing around watching it happen with the polite detachment of people waiting for a particularly dull bus. We call ourselves socialists. We pat ourselves on the back for healthcare and parental leave and dental care—and yes, these are good things, genuinely good things—but then we turn around and tax cryptocurrency and used cars while allowing housing prices to reach heights so absurd that Marie Antoinette would blush at the audacity.

“Let them rent apartments made of pressed wood chips,” our leaders might as well say, if they said anything honest at all.

Here’s the thing about Canada that makes this whole mess particularly rich: we have land. Gobs of it. Mountains of it. Prairies stretching farther than the eye can see, forests dense enough to hide entire logging companies, and cities—oh, the cities—surrounded by sprawl potential that would make a Texas developer weep with joy. And yet, somehow, somehow, we’ve managed to create a housing crisis that rivals nations built on rocky islands and ancient city-states where Napoleon once took a piss.

It’s like starving to death in a grocery store.

The Numbers Don’t Lie (Though Our Politicians Try)

Let me paint you a picture with actual numbers, because unlike most political promises, numbers have the decency to stay still when you look at them.

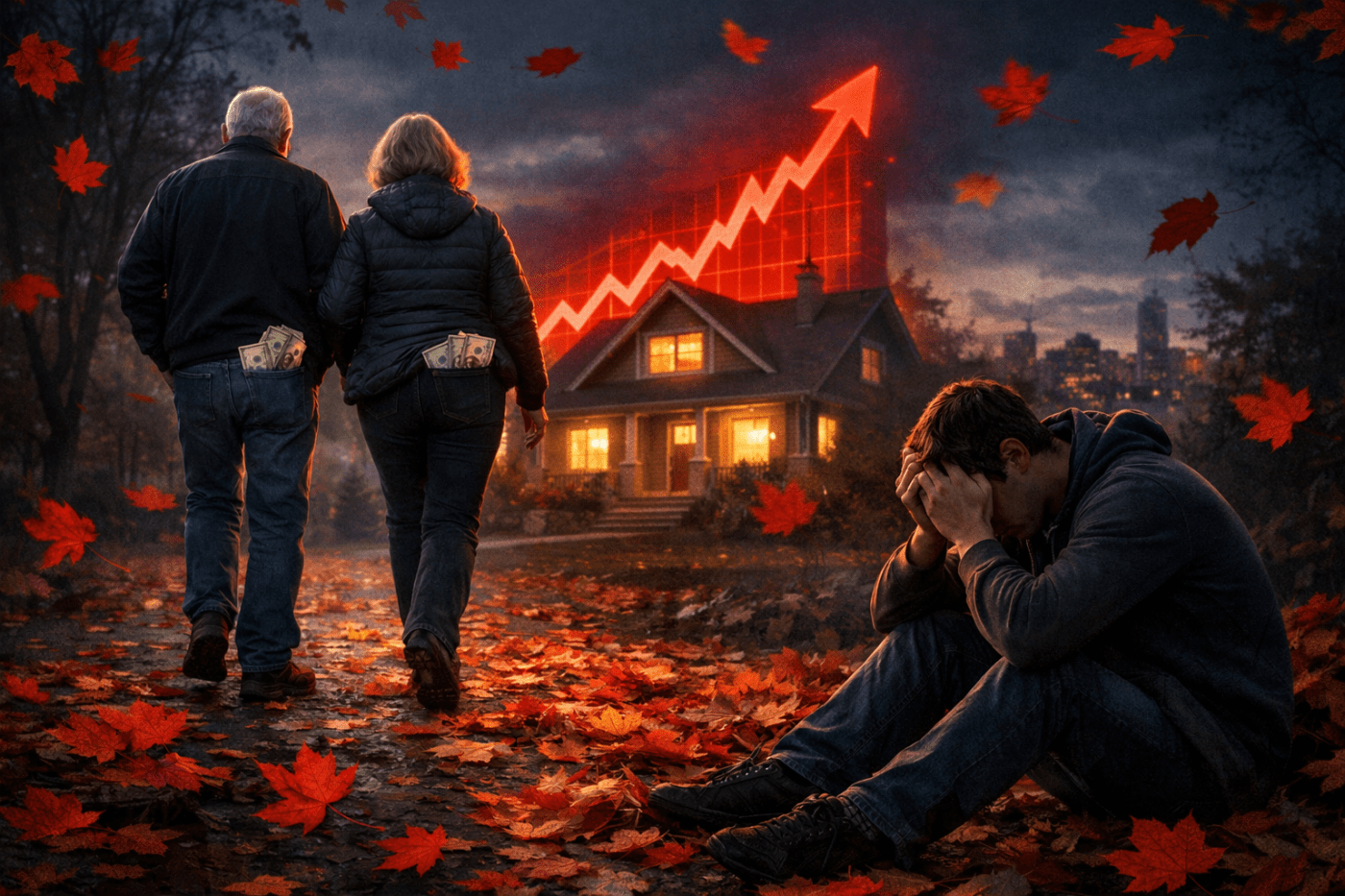

From 2021 to 2024, Canadian home prices surged approximately 35% in major urban centers. Yes, you read that right. Thirty-five percent. In three years. For homes. The things that were already unaffordable. But that’s just the cherry on top of a very expensive sundae. Over the past decade, average home prices in Canada have climbed roughly 150%—effectively doubling and then some—while wages have crawled upward at a pace that would embarrass a particularly lazy snail.

A typical home in Vancouver now costs around $1.2 million. In Toronto, you’re looking at over $1.1 million. Even in cities that nobody outside Canada has heard of, prices have shot through the roof like they’ve been launched from a cannon made of pure speculation and regulatory failure.

And apartments? Duplexes? The “affordable” options? They’ve followed the same trajectory, soaring 30-40% in many markets since 2021 alone. Meanwhile, millennials and Gen Z—the people who are supposed to be building this country’s future—watch from the sidelines like kids pressing their noses against the window of a candy store they’ll never be allowed to enter.

The Land Trap Snaps Shut

Mike Bird, in his book The Land Trap, explains what’s happening with the kind of clarity that makes you wonder why nobody in government seems to have read it. Land, unlike every other asset in the known universe, doesn’t depreciate. Houses fall apart. Ideas become obsolete. But land? Land just sits there, getting more valuable as everything around it gets built up, improved, and invested in—none of which the landowner had to do themselves.

It’s the world’s greatest passive income scheme, and Canada has turned it into our national religion.

Here’s where it gets perverse: for decades, banks have used home equity as the primary collateral for small business loans. Got a good idea? An innovative product? A dream that could employ dozens of people and generate real economic value? Well, you’d better own a house first, because without that collateral, you’re not getting a loan. We’ve essentially told an entire generation: “Your ideas don’t matter. Your work ethic doesn’t matter. Your potential doesn’t matter. What matters is whether your parents helped you buy a house in 2015.”

This is how economies die, by the way. Not with a bang, but with a million entrepreneurs who never got the chance to try.

The Boomers Are Coming From Inside the House

Now, let’s talk about the elephant in the room—or rather, the Boomer in the four-bedroom suburban home they bought for $80,000 in 1985 that’s now worth $1.5 million.

From their perspective, everything is working exactly as it should. They bought when buying was possible. They saved and invested. They played by the rules of their time, and those rules rewarded them handsomely. Their homes have become their retirement funds, their children’s inheritance, their proof that the system works.

And here’s the uncomfortable truth: they’re not wrong to feel this way. We told them for fifty years that homeownership was the path to security, the foundation of middle-class prosperity, the single smartest investment they could make. And it was for them.

But now we’re trapped in a prisoner’s dilemma of epic proportions. Any policy that makes housing affordable for young people necessarily reduces the value of existing homes. And existing homeowners vote. They vote a lot. They also control most of the wealth, sit on most of the city councils, and have the most to lose from change.

So when a politician proposes anything that might actually address housing affordability—denser zoning, higher property taxes, ending speculation—homeowners rise up like an army of khaki-wearing warriors defending their nest eggs. “Think of the neighbourhood character!” they cry. “Think of the property values!” What they mean is: “I’ve got mine, and I’ll be damned if I let you change the rules now.”

It’s like raising a child, telling them you love them, then when they grow up, refusing to invite them to Thanksgiving and Christmas and bashing them behind their back because they voted for the other party. Madness.

The Socialist Country That Forgot How to Share

Canada loves to think of itself as a kinder, gentler nation. We have socialized medicine. We have generous parental leave. We even have dental care now, for crying out loud. But when it comes to land—the single most important asset for building wealth and economic opportunity—we’ve adopted a philosophy that makes American capitalism look downright charitable.

We tax everything. Cryptocurrency gains? Taxed. Bought a used car? Taxed. Made money on stocks? Taxed. Hell, we’ll tax you for having the audacity to die with assets left over. But housing appreciation? The thing making millionaires out of people whose only skill was being born at the right time? That gets special treatment. Principal residence exemption. Generous deductions. Policies designed to make land the single most attractive investment in the country.

And then we wonder why everyone’s treating homes like stocks instead of places to live.

Meanwhile, young Canadians are making a calculation that any rational person would make: if I can’t afford to live here, I’ll go somewhere I can. They’re moving to the U.S., where wages are higher, and homes are (relatively) cheaper. They’re moving to Europe, to Asia, to anywhere that doesn’t require them to spend 60% of their income on a one-bedroom apartment made of oriented strand board—that’s OSB, wood chips and glue pressed together, the construction material equivalent of saying “close enough.”

And yes, let’s talk about OSB for a moment, because it’s a perfect metaphor for everything wrong here. We’re cramming families into cheap apartments constructed with materials that off-gas chemicals, provide minimal insulation, and will need major repairs within twenty years. But hey, at least developers are making healthy profit margins on these tinderboxes while families tell themselves they’re “getting into the market.”

It’s like being invited to dinner and being served a picture of food.

Who Benefits? Follow the Money (Or Don’t, Because It’s Depressing)

Let’s be crystal clear about who wins in this system:

Landowners. Anyone who bought before 2010 has watched their net worth explode without lifting a finger. Their homes have become piggy banks that refill themselves automatically.

Developers. Building cheap apartments with OSB and selling them at premium prices is a business model so profitable it makes cryptocurrency look like a savings account.

Banks. They’ve slowly transformed from institutions that fund businesses into mortgage originators. Why take a risk on a startup when you can make endless low-risk loans backed by ever-appreciating land?

Established wealthy families. They can afford to buy investment properties, to help their kids get into the market, to play the game at a level young people can’t even observe, let alone participate in.

Who loses? Everyone else. Especially young people. Especially people with ideas but no inheritance. Especially the entrepreneurs who could build the next great Canadian company if only they could get a loan without first owning a million-dollar home.

The Economic Time Bomb Nobody Wants to Discuss

Here’s what keeps me up at night, and what should terrify every Canadian leader who’s paying attention:

When young people can’t afford to live somewhere, they leave. When talented people leave, innovation leaves. When innovation leaves, economic growth dies. This isn’t speculation—it’s cause and effect as reliable as gravity.

History has shown us this pattern before. After the Hundred Years’ War devastated Europe, millions fled to the Americas. Why? Because the old world had become a place where land was locked up by aristocrats, where opportunity was strangled by entrenched interests, where the young had no path to prosperity except through inheritance or revolution. They left for places where land was available, where work could lead to ownership, where a person could build something without first needing to be born into the right family. Sound familiar? We’re watching the same exodus happen in slow motion, except now Canadians are leaving for Texas and Arizona instead of crossing the Atlantic. The only difference is that this time, we’re doing it to ourselves on purpose.

But here’s an even darker twist: the people who do stay aren’t having children. Canada’s birth rate has plummeted to 1.33 children per woman—well below the 2.1 needed to maintain the population. Why? Because people living in $2,500-a-month one-bedroom apartments can barely afford to feed themselves, let alone raise children. You need a second bedroom for a baby, which means another $1,000 a month. Daycare costs more than most people’s rent used to. It’s like asking someone to start a family in a lifeboat that’s already taking on water.

So what’s Canada’s solution? Fling open the immigration doors and hope that newcomers from other countries will fill the demographic hole our housing policy created. We’re essentially running a Ponzi scheme where we need constant waves of new entrants to keep the economy functioning because we’ve made it financially suicidal for our existing citizens to reproduce. It’s like a restaurant that has to keep finding new customers because it keeps poisoning the regulars.

Canada is already seeing this perfect storm. Our best and brightest increasingly look south, where tech salaries are double and homes cost half as much. Our entrepreneurs increasingly struggle to secure funding because they lack collateral in a banking system that’s forgotten how to evaluate anything except real estate. And our young couples are choosing between homeownership and children—a choice no prosperous nation should force its citizens to make.

And here’s the kicker: Canada’s comparative advantages—natural resources, educated population, political stability—don’t mean squat if nobody can afford to live here. You can’t build a knowledge economy if your knowledge workers are living in Portland and Sydney, and Austin.

We’re also building a two-tier society with the efficiency of a Soviet planning committee. The established wealthy on one side, with their appreciated homes and rental properties. And everyone else on the other, paying ever-increasing rents to the first group, unable to build wealth, unable to take risks, unable to do anything except work until they’re too old to remember why they bothered.

This is economic suicide dressed up as fiscal responsibility.

What the Hell Do We Do About It?

Now we come to the hard part, where pointing out problems gives way to proposing solutions that will make everyone angry.

First: Tax land, not improvements. Implement a genuine land value tax that makes holding property expensive enough to discourage speculation but doesn’t penalize people for building or improving. This is basic economics—tax the thing you want less of (speculation), not the thing you want more of (housing construction).

Second: End the principal residence exemption, gradually. Yes, this will anger homeowners. Yes, this will require a transition period measured in years, not months. But we cannot continue to treat housing appreciation as tax-free income while taxing actual productive work. Phase it in slowly, with generous exemptions for seniors and low-income families. But do it.

Third: Look to Singapore. Yes, I know, comparing Canada to a city-state feels absurd. But Singapore solved this problem by having the government acquire approximately 90% of the land and provide high-quality, low-cost public housing through 99-year leases. Citizens can buy one flat, noncitizens are restricted from the market, and prices stay rational. We don’t need to copy this exactly, but we need to learn from it: when you treat housing as infrastructure instead of investment vehicles, you can have affordability without sacrificing quality.

Fourth: Massive upzoning around transit. Every major city should allow four to six-story buildings within walking distance of rapid transit. No exceptions for “neighbourhood character.” Build up, build dense, build now.

Fifth: Federal intervention in municipal zoning. Cities have proven they can’t or won’t solve this themselves. The federal government needs to tie infrastructure funding to housing targets and zoning reform. No more highways and transit lines for cities that refuse to build housing.

Sixth: Public banking infrastructure for business lending. If private banks have abandoned business lending in favour of mortgages, create public alternatives that evaluate entrepreneurs on their ideas and potential, not their property holdings.

Seventh: Ban corporate ownership of single-family homes. Companies buying houses to rent them back to families is feudalism with better PR. Stop it.

The Choice Before Us

So it goes.

Canada stands at a crossroads, though you wouldn’t know it from the tepid response of our leaders. One path leads to a country that remembers what made it great: opportunity, possibility, the genuine chance for people to build lives and businesses and futures. The other leads to a gated community with a flag, where only the established and wealthy can afford to stay, and nine months of winter keep the riff-raff away.

We can continue pretending we’re a socialist country while running an economic system that would make robber barons blush. We can keep taxing cryptocurrencies and used cars while treating housing speculation as a sacred right. We can keep building cheap apartments from wood chips and calling it progress.

Or we can do something radical: we can decide that land, in a country with more of it than almost anywhere on Earth, shouldn’t be the thing that determines who gets to participate in the economy.

The clock is ticking. Young people are leaving. Entrepreneurs are giving up. The future is packing its bags and looking at real estate listings in other countries.

Our leaders need to act, and they need to act soon. Not with studies or committees or consultation periods measured in years. With an actual policy that actually makes housing affordable for actual people who actually want to live here.

Because right now, we’re teaching our young people a lesson they’ll never forget: Canada is a wonderful place to be from. Just don’t try to stay here.

And so it goes.

Leave a comment