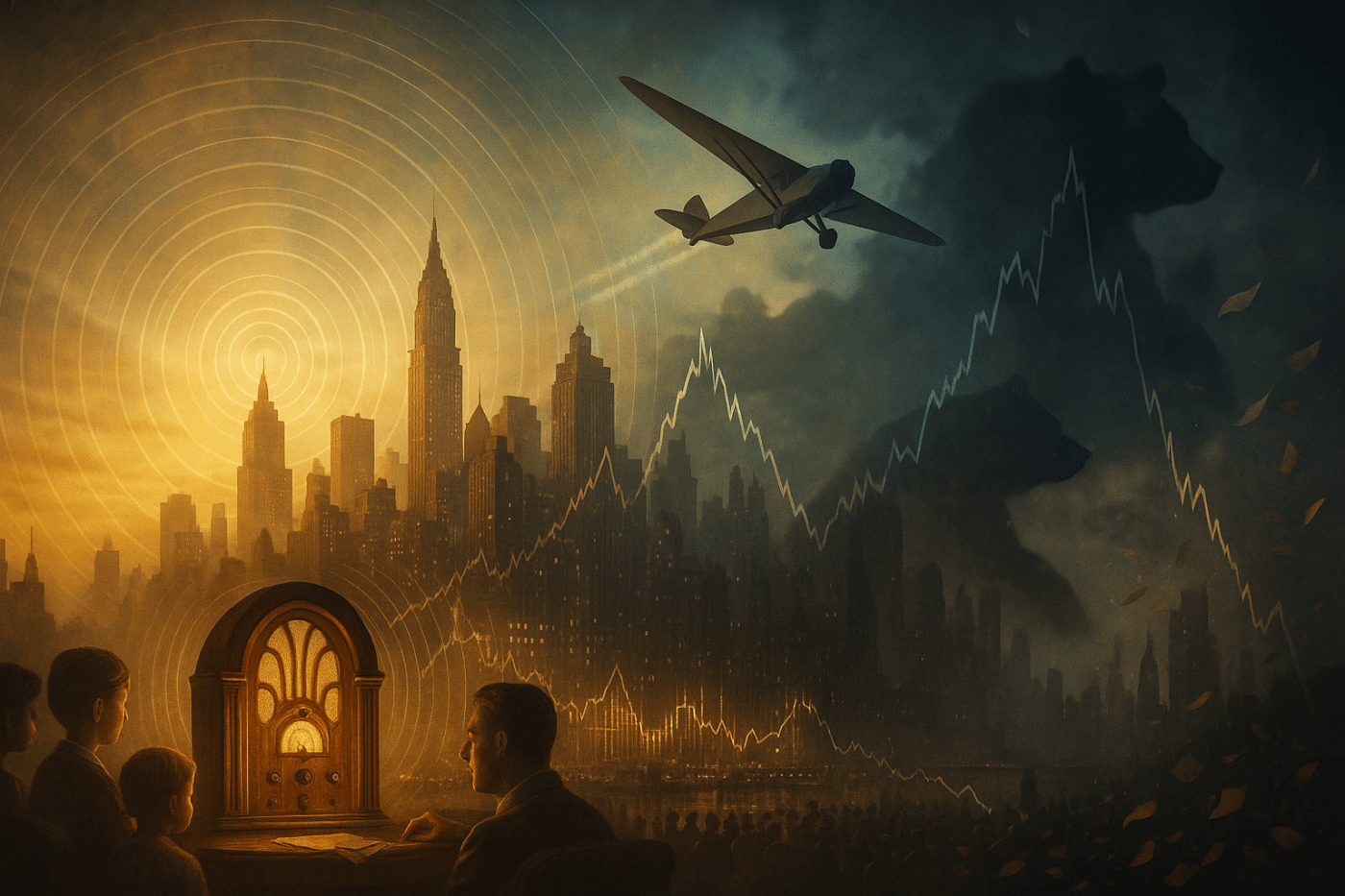

May 21, 1927. 5:52 AM. Paris.

A man climbs out of a silver airplane at Le Bourget Field, and 150,000 people surge forward like a wave breaking. Women weep. Grown men stand frozen, hands pressed to their chests. Charles Lindbergh has just flown 3,600 miles alone across an ocean that had swallowed so many before him, and in this moment, everything—everything—seems possible.

Back in New York, ticker tape will fall like snow for days. Stock tickers in brokerage houses will hammer out the news: aviation stocks up 20%, 30%, 50%. Men in wool suits will lean forward in their chairs, eyes bright with something between greed and genuine wonder, and they will believe they’re watching the future arrive ahead of schedule.

Herbert Hoover, soon to be president, watches all of this and sees destiny. American ingenuity conquering the sky. Prosperity without end. A future so certain you could bet the mortgage on it.

What he doesn’t see—what nobody wants to see when they’re drunk on the future—is that gravity works on markets the same way it works on everything else.

Then.

It’s 2025, and I’m staring at my portfolio at 6:30 AM, and we’re doing it all over again.

The Dance: When Optimism Meets Gravity

Before becoming synonymous with breadlines, Herbert Hoover was considered a genius. A self-made mining engineer. A humanitarian who’d fed millions in war-torn Europe. As Secretary of Commerce, he’d built the radio and aviation industries—the transformative innovations of his age. When he won the presidency in 1928, people believed poverty itself might soon be obsolete. The stock market had tripled in five years.

Sound familiar?

When the crash came, Hoover took unprecedented action: tax cuts, massive public works, creating the ‘Reconstruction Finance Corporation’, and increasing federal spending by 48 percent. He ran deficits larger than Roosevelt’s early years. None of it mattered. The bubble had inflated beyond what any intervention could deflate. He’d confused the promise of technology with the promise of endless returns.

Donald Trump stands in a similar spotlight to artificial intelligence. Both men share a peculiar American optimism: that technology and capitalism guarantee each other’s prosperity. Both wrapped themselves in economic nationalism—America First, then and now. Both championed transformative technologies with genuine enthusiasm.

But here’s the critical difference: Hoover maintained distance from the industries he’d helped build. Trump is surrounded by tech CEOs with billions riding on the AI narrative—Elon Musk with his own AI company, executives who need the money to keep flowing. These aren’t advisors; they’re stakeholders manipulating policy for self-interest.

The 8 Out of 8

Economists Brent Goldfarb and David Kirsch studied 58 historical bubbles and developed a framework scoring them 0 to 8. AI scores an 8—maximum bubble conditions.

Uncertainty? Three years after ChatGPT’s launch, nobody can articulate a sustainable business model. OpenAI’s Sam Altman once told investors his plan was to build AGI and simply ask it how to make money. A MIT study found 95 percent of firms adopting AI saw zero profit.

Pure plays? Nvidia became more valuable than Canada’s entire economy. It invests $100 billion in OpenAI, which buys Nvidia chips, which increases Nvidia’s value—a perfect feedback loop to nowhere. These firms are increasingly intertwined: Nvidia invests in OpenAI, which relies on Nvidia chips, which rely on Microsoft’s computing, which relies on OpenAI’s models. A house of cards built by architects who all invested in each other’s construction companies.

Novice investors? In 2024, Nvidia was the most-bought stock by retail traders on Robinhood, who pumped $30 billion into the company. TikTok influencers hawk AI stocks as guaranteed wealth. The rags-to-riches dream lives again.

Great narrative? AI will cure cancer, solve climate change, and automate all jobs. We must beat China to AGI. Don’t regulate it. Don’t slow down. Just believe.

It’s a narrative so seductive that it makes aviation and radio bubbles look quaint. At least we knew what airplanes and radios did.

The Puppet Masters

In the 1920s, Charles “Sunshine Charley” Mitchell ran National City Bank and democratized speculation, selling securities to masses chasing prosperity.

He defied the Federal Reserve’s warnings about excessive speculation. In March 1929, when the Fed tried to curb it, Mitchell announced his bank would provide $25 million in credit to keep the party going. He became a folk hero.

When it crashed, National City’s worthless bonds destroyed mom-and-pop investors while executives walked away rich. The democratization of speculation became the democratization of loss.

Today it’s Jensen Huang, Nvidia’s CEO, whose keynotes are treated as prophetic visions. Like Mitchell, he sits at the center of interconnected bets. Unlike Mitchell, he whispers directly into presidential ears.

Why This Time Is Worse

In 1929, money poured into anything with “radio” or “aviation” in its name, regardless of business fundamentals. The spending was indiscriminate, frenzied, untethered from traditional metrics.

Today, slap “AI” on your pitch deck and watch billions flow. The pattern is identical.

But radio and aviation were single industries. AI is being sold as total social transformation—integrating into every industry, every economy, every aspect of society simultaneously. This isn’t a sector bubble. It’s a bubble in the idea of the future itself.

In 1919, RCA began broadcasting and the world had never seen anything like it. Voices traveling through the air without wires seemed like sorcery. By 1929, RCA was the most heavily traded stock alongside Ford Motor Company—the Nvidia of its day. Then came October 1929. By May 1932, radio stocks had lost 97 percent of their value.

Aviation followed the same melody. Lindbergh’s flight was the ChatGPT moment of its era—the demonstration that made everything seem inevitable and imminent. From its 1929 peak, aviation stocks dropped 96 percent by 1932. Both technologies were real, transformative, miraculous. But the gap between promise and profit destroyed fortunes.

My Portfolio at 6:30 AM

Here’s the truth I don’t want to admit: I wake up at 6:30 AM sometimes and check my phone. Not because I’m expecting good news. Because I’m expecting the beginning of bad news.

My portfolio doesn’t have much direct AI exposure. I learned something from the dotcom crash. But “not much direct exposure” means nothing in interconnected markets. Those managed funds? They’re betting on companies whose business models exist only in PowerPoint presentations.

Last week, Meta’s stock dropped 11 percent in a single day. $85 billion—gone. Is that the crack in the manifold?

Nvidia alone accounts for 8 percent of the entire stock market’s value. One company, making chips for an industry that can’t explain how it plans to make money. If Nvidia catches a cold, your portfolio gets pneumonia.

The Depression that started in 1929 wasn’t just about stock traders. It was about systemic collapse. The interconnectedness of speculation created a cascade of failure—banks, farms, businesses, lives. People who’d never owned a share of RCA stock found themselves in breadlines because the grocer couldn’t get credit because the bank had invested too heavily in aviation stocks.

Radio and aviation were just two ingredients in that toxic recipe. I lie awake doing the math on how many ingredients we’re mixing this time.

What We Know But Pretend Not To

I don’t know exactly when this bubble bursts. Nobody does. That’s what keeps people in the game long past when they should have cashed out.

Maybe it’s months away. Maybe years. Maybe some breakthrough will soften the landing from catastrophic to merely devastating. Technology does sometimes deliver, just rarely on the timeline speculation demands.

What I do know: we’re watching an 8 out of 8 on the bubble scale. Investment patterns mirror the most catastrophic market failures in history. Companies burn billions with no path to profitability while retail investors pour savings into AI stocks because Robinhood made it as easy as ordering pizza. The narrative of inevitability drowns out every voice of caution.

Hoover was caught between knowing the market was overheated and believing the technological transformation justified the optimism. He was right about the technology and wrong about the timeline. That gap destroyed his presidency.

We’re nearly a century later with different technology, same dance, same music building to the same crescendo.

The Lesson We Never Learn

There’s a photograph from 1929 I think about. Black Thursday. October 24th. Crowds outside the New York Stock Exchange. The faces are blurred by long exposure, but you can read the posture—hats tilted at angles suggesting desperation or disbelief.

Somewhere in that crowd is someone who’d mortgaged the house to buy aviation stocks because Lindbergh flew to Paris. Someone who’d invested their children’s education fund in radio companies because voices through the air would obviously change everything.

That person was right. Radio did change everything. Aviation did revolutionize the world. They were right about the technology and wrong about the timing, and that gap destroyed them anyway.

The technology my grandmother’s father wept over hearing for the first time, is the same technology I use without a second thought. Radio didn’t fail. The miracle was real. But the belief that miracles arrive on schedule and pay dividends quarterly—that’s what failed. That’s what always fails.

We’re building the same miracle again, the same tragedy. Somewhere right now, someone is watching AI generate an image and feeling genuine wonder at what humans can create.

And somewhere else, someone is looking at their Robinhood app, calculating how many Nvidia shares they can buy, believing the TikTok influencer who promised AI stocks are guaranteed wealth. They’re making the same fundamental mistake about the difference between a miracle and a return on investment.

I can’t tell you when the crash comes or how bad it will be. I can’t promise I’ll be smart enough to get out before it happens—my portfolio keeps me up for a reason.

But I can tell you this: when we’re standing in the rubble, sorting through the wreckage of 401(k)s and pension funds and retirement dreams, we’ll know exactly how. We’ll have the history books. We’ll have the pattern. We’ll have scholars like Goldfarb and Kirsch who told us in plain language.

We’ll have everything we need to understand what happened, except the wisdom to have stopped it before it started.

Mark Twain survived the Panic of 1873 and said history doesn’t repeat itself, but it rhymes. We’re not replaying 1929 exactly. But the rhythm is identical: pride, narrative, speculation, indiscriminate spending, inevitability, crash.

The future is still coming. AI will transform the world. The miracle is real.

It’s just the price tag that’s fiction. And the timeline is fantasy.

And we’re all going to pay for those fictions, whether we bought stock or not. Because that’s how bubbles work. That’s how the gap between wonder and profit has always worked, from radio to aviation to dotcom to AI.

The bigger they are, after all, the harder we fall.

May 21, 1927. 5:52 AM. Paris. A man climbs out of a silver airplane, and 150,000 people surge forward like a wave breaking, and everyone believes the future has finally arrived.

They were right. They just didn’t know it would take forty years and a depression to get there.

We never do.

Leave a comment